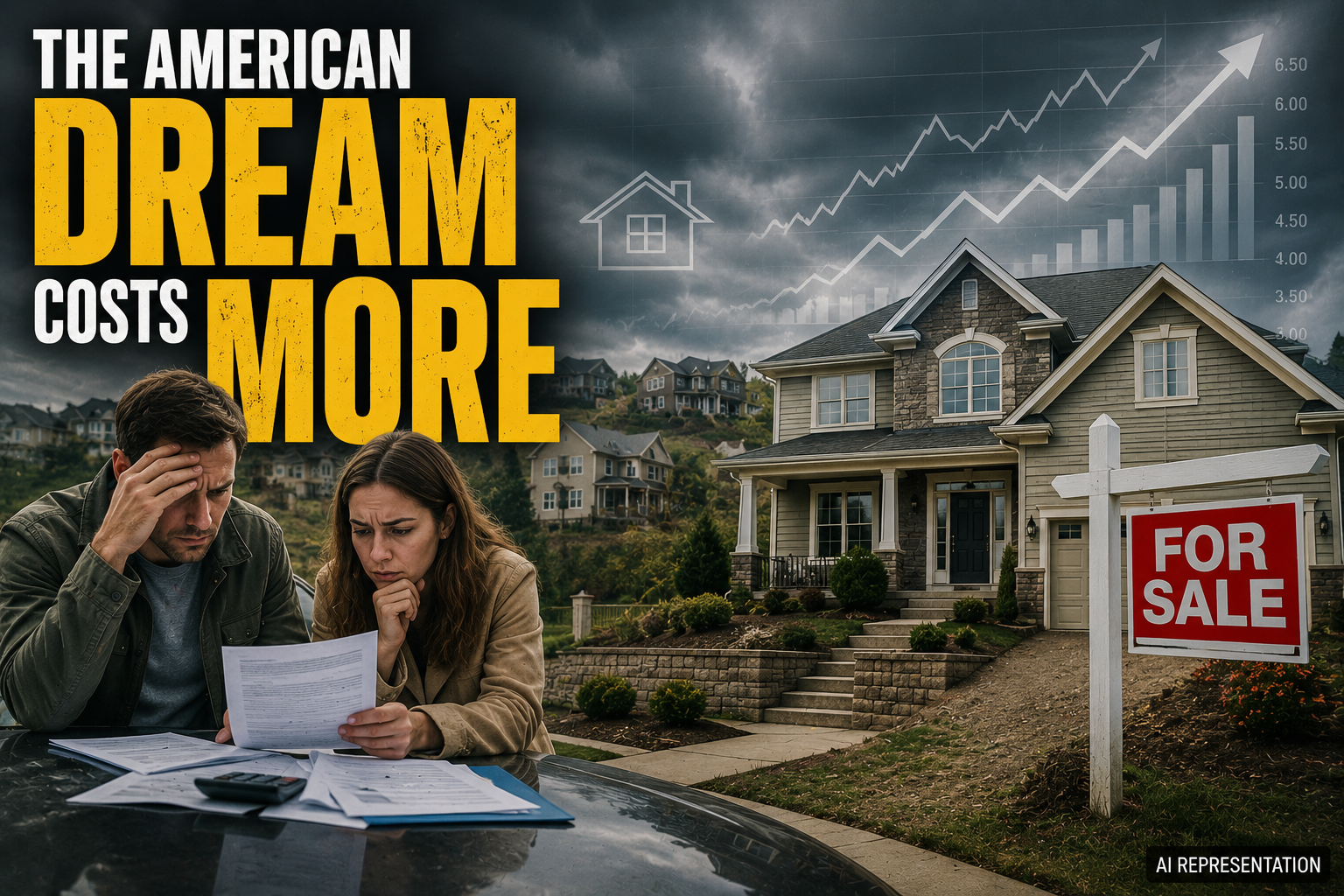

The American Dream Is Getting More Expensive—and Even Six-Figure Salaries Aren’t Enough

A six-figure salary once signaled financial security in much of America. Today, it may not be enough to comfortably buy a home.

Across large parts of the United States, families earning well above the national median income are finding themselves priced out of the housing market. The challenge is no longer limited to low-income households or first-time buyers. Increasingly, professionals, dual-income families, and even households earning more than $100,000 a year are discovering that homeownership has become far harder than previous generations experienced.

The question is no longer why low-income Americans cannot afford homes. The more surprising question is why many high-income Americans cannot either.

What Happened

The affordability problem is being driven by a combination of factors rather than a single shock.

Home prices surged during and after the COVID-19 pandemic, while mortgage rates rose sharply following efforts to control inflation. Although mortgage rates have fluctuated, they remain significantly higher than the ultra-low levels seen during 2020 and 2021. Recent data showed the average 30-year fixed mortgage rate climbing above 6.5%, adding substantial costs to monthly payments.

At the same time, housing supply remains constrained. Experts note that the United States has failed to build enough homes for years, creating a shortage that continues to push prices upward. Estimates cited by housing researchers suggest the country remains millions of housing units short of existing demand.

The result is a market where buyers face both expensive homes and expensive financing.

Background

America’s housing challenge did not emerge overnight.

Following the 2008 financial crisis, homebuilding slowed dramatically and remained below historical levels for years. As the economy recovered, population growth and household formation gradually outpaced new construction in many regions.

During the pandemic, demand for larger homes increased as remote work became common. At the same time, historically low interest rates encouraged home purchases and pushed prices higher. When inflation later surged, borrowing costs increased rapidly, but home prices did not fall enough to offset the impact of higher mortgage rates.

Many homeowners who secured mortgages below 5 percent are now reluctant to sell and take on significantly higher borrowing costs. This “lock-in effect” has reduced the number of homes available for sale and further tightened supply.

Why It Matters

Housing is often the largest financial decision a household makes.

When homeownership becomes unaffordable, the effects spread far beyond the property market. Families delay major life decisions, including marriage, relocation, and retirement planning. Workers may be unable to move to cities with better job opportunities because housing costs are too high.

Businesses can also be affected. Employers in expensive regions often struggle to attract workers who cannot afford to live nearby. Local economies may experience reduced mobility as people remain in areas where they already own homes rather than moving to where jobs are growing.

The affordability crisis also widens wealth gaps. Homeownership has historically been one of the primary ways American families build long-term wealth. If fewer households can buy homes, future wealth creation may become increasingly concentrated among those who already own property.

Analysis

The most important insight is that America’s housing crisis is no longer simply a low-income problem.

Traditionally, affordability challenges were concentrated in cities such as New York, San Francisco, and Los Angeles. Today, many previously affordable markets are experiencing similar pressures. Researchers have noted that Sun Belt cities such as Miami and Phoenix increasingly resemble traditionally expensive coastal housing markets.

Another important shift is that affordability is being driven as much by financing costs as by home prices. A buyer may qualify for a mortgage on paper, but monthly payments can still consume a large share of income because of elevated interest rates. Recent data show debt-to-income ratios rising and borrowers contributing larger down payments simply to keep monthly costs manageable.

Perhaps the clearest sign of the problem is behavioral change. Research indicates that prospective buyers are increasingly targeting smaller homes than they would have purchased in the past. Rather than moving up the property ladder, many are lowering expectations to remain within budget.

The deeper issue is structural. High interest rates may eventually fall, but a shortage of housing supply takes years to resolve. Unless construction significantly outpaces current levels, affordability pressures could persist even if borrowing costs ease.

For India, the story offers an important lesson. Housing affordability problems often develop slowly and become visible only after years of underbuilding and rising land costs. Once supply shortages become entrenched, reversing them is far more difficult than preventing them.

Conclusion

The American Dream was once built around a simple idea: work hard, earn a good income, and eventually buy a home.

For a growing number of Americans, even that formula is no longer working as expected.

The affordability crisis is not merely about expensive houses. It is the result of years of limited housing construction, rising borrowing costs, and a market that increasingly favors existing homeowners over new buyers. Until supply expands meaningfully or costs decline substantially, even many high-income households may continue to find that owning a home remains just out of reach.

With AI inputs.