A regulatory investigation involving Bengaluru-based Rajesh Exports has rapidly become one of the most closely watched corporate governance stories in India.

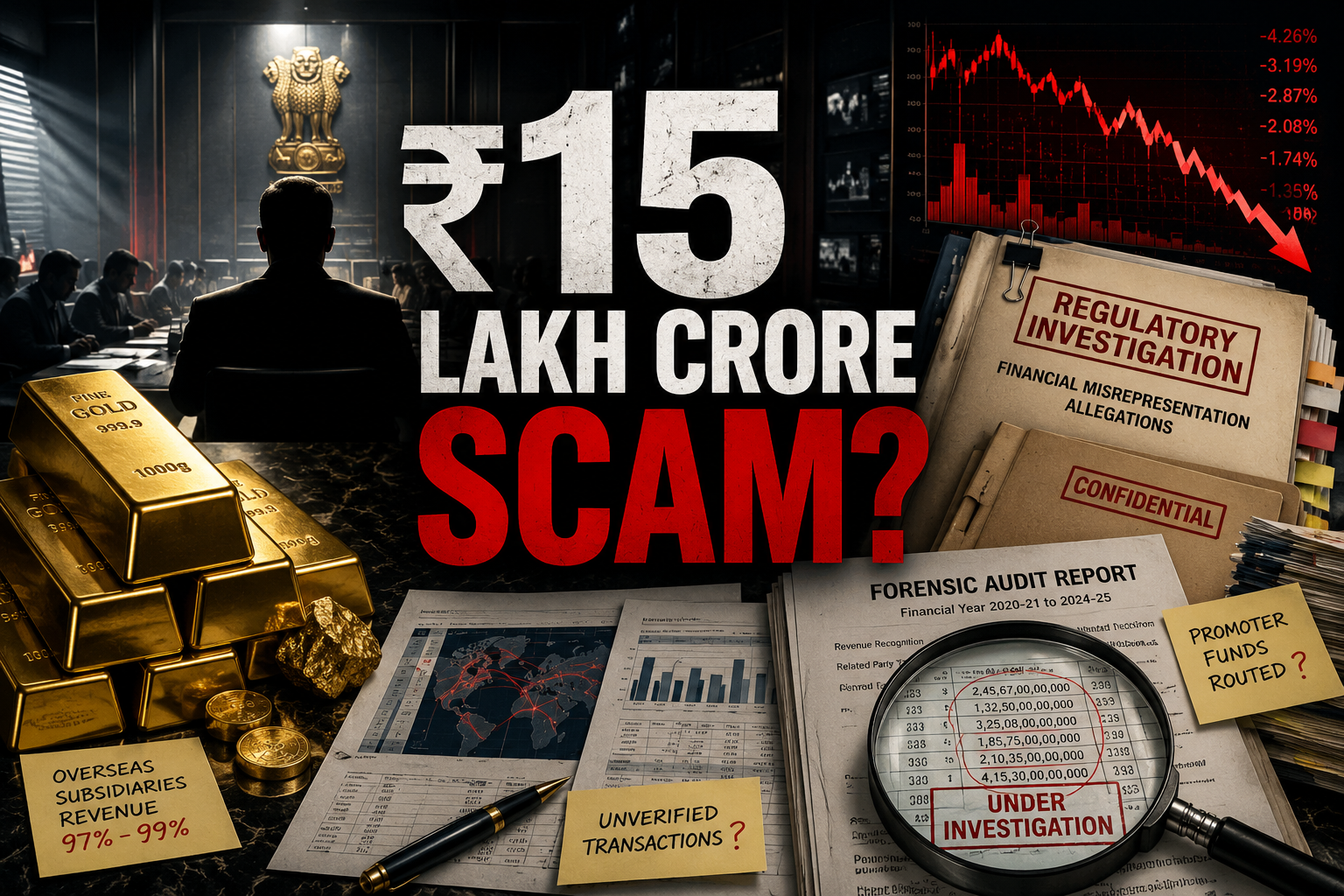

At the center of the controversy is an interim order issued by the Securities and Exchange Board of India (SEBI), which alleges that the company may have misrepresented approximately ₹15.15 lakh crore in revenues over multiple financial years.

The allegations are extraordinary not only because of the size of the numbers involved, but because they raise broader questions about how large multinational corporate structures are reported, audited, and monitored.

The company has denied wrongdoing and stated that the regulator’s observations arise from what it describes as confusion regarding revenue reporting associated with its overseas operations.

As the investigation continues, the key question for investors is simple: Is this a case of accounting interpretation, disclosure failure, or something more serious?

What Happened

On June 3, 2026, SEBI issued an interim order against Rajesh Exports Limited and its Chairman and Managing Director Rajesh Mehta as part of an ongoing investigation.

According to the regulator, approximately 97% to 99% of the company’s reported consolidated revenue during the period under review was attributed to overseas subsidiaries, particularly Switzerland-based Valcambi SA.

SEBI alleged that around ₹15.15 lakh crore in reported revenues between FY2020-21 and FY2024-25 may have been misrepresented through disclosures linked to overseas entities.

The regulator further alleged:

• Revenue figures could not be adequately supported through verifiable records requested during the investigation.

• Certain transactions involving an entity named Affluence Shares and Stocks Private Limited appeared inconsistent with available records.

• Company funds may have been routed through promoter-linked accounts without required approvals or disclosures.

• Related-party transaction disclosures may have been inadequate.

Based on its preliminary findings, SEBI barred Rajesh Mehta and imposed interim restrictions while the investigation continues.

Rajesh Exports has disputed the allegations and stated that its revenues are correctly reported. The company has argued that the issue largely relates to differences in understanding revenue disclosures associated with Valcambi and has said it intends to provide additional documentation and clarification.

Importantly, the matter remains under investigation, and no final determination has yet been made.

Background

Rajesh Exports is among India’s most recognized gold refining and jewellery companies.

The company operates across refining, manufacturing, and retail segments and gained international prominence after acquiring Swiss precious metals refiner Valcambi in 2015.

For years, Rajesh Exports reported some of the highest revenue figures among listed Indian companies.

However, according to SEBI’s interim findings, a significant portion of those revenues originated from overseas subsidiaries rather than the listed Indian entity itself.

The investigation reportedly began after concerns were raised regarding long-outstanding receivables and the verification of large-scale transactions.

As the probe expanded, regulators sought customer-level data, vendor records, transaction documents, subsidiary financial information, and audit trails.

According to the interim order, several records requested by investigators could not be fully verified or were allegedly not provided in complete form.

That transformed what initially appeared to be an accounting review into a broader examination of corporate disclosures and governance practices.

Why It Matters

The Rajesh Exports case extends far beyond a single company.

For investors, the issue highlights the risks of relying solely on headline revenue figures without understanding where those revenues originate and how they are generated.

For regulators, the matter tests India’s ability to monitor increasingly complex multinational corporate structures.

For listed companies, the investigation reinforces the growing expectation that disclosures must be transparent, verifiable, and capable of withstanding forensic scrutiny.

For auditors and boards of directors, the allegations raise questions about oversight responsibilities, especially when substantial portions of a company’s business are conducted through overseas subsidiaries.

The case also affects market confidence. Large listed firms often attract investments from retail investors, mutual funds, insurers, and foreign institutions. When major accounting questions emerge, the impact can extend far beyond a single stock.

Analysis

The most important aspect of the Rajesh Exports controversy is not the headline number.

It is the structural issue underneath it.

Modern corporations frequently operate through global subsidiaries spread across multiple jurisdictions. Investors typically rely on consolidated financial statements to understand the overall business.

The challenge emerges when a significant portion of reported activity exists outside the immediate visibility of shareholders and regulators.

SEBI’s allegations suggest a potential mismatch between reported consolidated revenues and the availability of independently verifiable supporting records.

If regulators ultimately substantiate these allegations, the case could become a landmark example of why disclosure quality matters as much as disclosure quantity.

A second lesson involves corporate governance.

The investigation places renewed focus on related-party transactions, promoter influence, board oversight, and internal controls. These are recurring themes in many major corporate controversies globally.

Third, the case highlights a growing trend in Indian markets: increased reliance on forensic audits and data-driven investigations rather than traditional compliance reviews.

Regulators are increasingly examining transaction-level evidence instead of relying solely on audited financial statements.

Historically, major market scandals often lead to stronger disclosure norms and tighter compliance requirements. Whether this case results in similar reforms will depend on the final findings.

At present, the allegations remain preliminary, but the regulatory response signals that oversight standards are becoming more stringent.

MARKET IMPACT

The immediate market impact has been significant.

Following SEBI’s interim order, Rajesh Exports shares came under pressure as investors reacted to the scale of the allegations and uncertainty surrounding future developments.

The case may also influence broader investor sentiment regarding companies with complex overseas structures and unusually large revenue figures.

Institutional investors are likely to pay closer attention to subsidiary disclosures, audit quality, and transaction transparency in future evaluations.

INVESTIGATION STATUS

Current Status: Ongoing (till the time of publishing this article)

According to SEBI’s interim order:

• Investigation remains active.

• Interim restrictions have been imposed.

• Additional scrutiny of financial statements, subsidiary records, and related-party transactions is continuing.

• Rajesh Exports has denied wrongdoing and stated it intends to respond with supporting documentation.

No final regulatory determination has been issued at the time of publication.

Conclusion

The Rajesh Exports controversy is ultimately about trust.

The investigation is testing whether reported financial performance accurately reflected underlying business activity and whether investors received a fair picture of the company’s operations.

While the allegations are serious, they remain allegations at this stage. The company’s response, the evidence presented during the investigation, and SEBI’s final findings will determine the eventual outcome.

Regardless of how the case concludes, it has already become an important reminder that in capital markets, transparency and verifiability matter just as much as growth and scale.

With AI inputs.